Systemic Denial Practices

Medicare Advantage Insurers Made Nearly 50 Million Prior Authorization Determinations in 2023

A KFFKFFKFF (formerly the Kaiser Family Foundation) is an independent, nonpartisan source of health-policy research, polling, and journalism. analysis found that Medicare Advantage insurers processed a staggering 49.8 million prior authorizationPrior AuthorizationA health-insurance process that requires your doctor to get advance approval from your plan before it will cover a specific service, procedure, or drug. requests in 2023 — up from 37 million in 2021 — averaging more than 4 requests for every single MA enrollee.

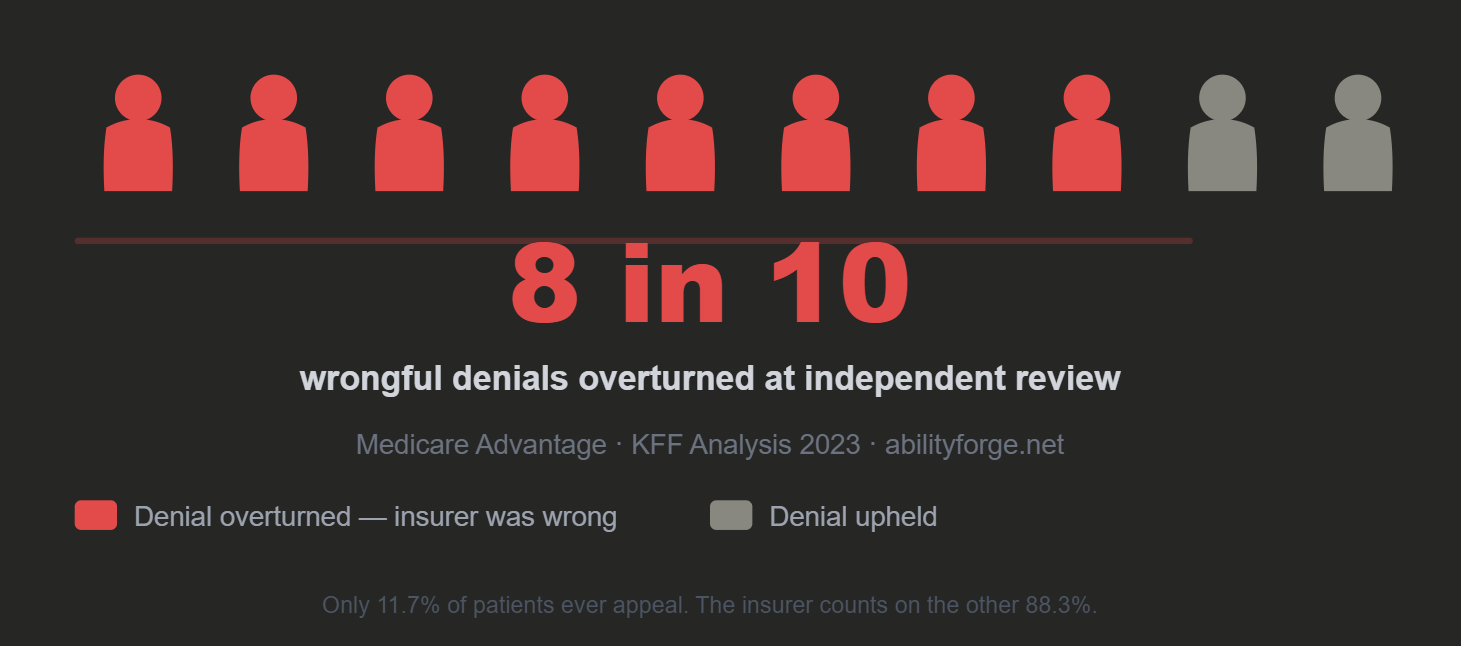

- Insurers denied 3.7 million requests. Only 11.7% of those denials were appealed — yet 81.7% of appealed denials were overturned in the patient's favor, suggesting millions of initial denials were improper.

- Total prior authorization requests: 49.8 million. Total denied: 3.7 million (7% of all requests).

- If 81.7% of all 3.7 million denials are as wrongful as those that were appealed, that is 3 million victims of the Denial Echo Chamber per year.

- Services with high denial rates included home health (15%) and skilled nursing facility stays (12%).

IRE Overturn Rates — The Insurers Above the Industry Average

Industry average: 81.7% of denied claims overturned at Independent Review. The following insurers exceed even that. These are not outliers — they are the top of a chart where the bottom is already indefensible.

93.6%

6.4% of denials upheld

89.7%

10.3% of denials upheld

86.0%

14% of denials upheld

These numbers have a specific meaning that gets lost in the abstraction of percentages. Centene issues a denial. An independent physician — with no financial stake in the outcome — reviews it. 93.6% of the time, that physician says Centene was wrong.

Centene knows this. Every insurer on this list knows their own overturn rate. They issue the denial anyway — because only 0.2% of patients ever appeal. For every 1,000 denials Centene issues, approximately 2 patients appeal, roughly 1.87 win, and 998 patients accept a denial that an independent physician would have overturned 936 times.

That is not a medical disagreement rate. That is a business model built on the near-certainty that patients will not fight back.

Read the KFF Article →

Read the KFF Article →

Claims Denials and Appeals in ACA Marketplace Plans in 2024

Insurers on the ACA Marketplace denied in-network claims at scale in 2024 — services already performed by an in-network doctor, retroactively denied. UnitedHealthcare remained above average at 33%.

- Consumers almost never appeal. Of denied in-network claims, patients filed formal appeals for less than 1%. When they did appeal, insurers upheld their own denial 56% of the time.

- The most common reason given for denial: "Other reason not listed" — 36% of all denials, 28,113,490 claims. No clinical rationale attached.

- "Administrative reason" accounted for another 25% — 19,612,209 claims. Together: 61% of denials with no medical explanation.

- "Not medically necessary" — the reason the public assumes is the primary driver — accounted for only 5% of denials.

- Blue Cross Blue Shield of Alabama denied 35% of in-network claims; UnitedHealth Group denied 33%.

Why Claims Are Really Being Denied — Myth vs. Reality

The public narrative focuses on "Not Medically Necessary" as the leading cause of denials. The data tells a different story. Here is what 2024 HealthCare.gov plan denials actually look like — every figure represents 5% of all denied claims.

The Common Assumption

other reasons...

Assumed #1 Cause

"Not Medically Necessary"

The public assumes this is the primary reason for denials.

"Other reason not listed. Administrative reason. That's how they twist it." — The denial reason breakdown, turned into a battle cry.

Consumer Survey Highlights Problems with Denied Health Insurance Claims

A KFF survey of insured adults found that nearly 1 in 5 (18%) reported having a claim denied in the past year. For those who experienced a denial, only 29% reported their "biggest problem" was ultimately resolved to their satisfaction.

- Among patients with a denied claim, 24% said their health declined as a result, and 24% said they were unable to receive care recommended by their doctor.

- 58% of all insured adults reported experiencing at least one problem with their insurance in the past year.

- Denials were most common for employer-sponsored plans (21%) and marketplace plans (20%).

- 69% of those with a denied claim didn't know they could appeal. 86% didn't know what government agency to contact for help.

⚠️ What These Statistics Look Like in Practice

The data above describes the systemic pattern. Here is what that pattern looks like when it lands on one person — and why the numbers above are not just statistics but a documented causal chain.

ApligrafApligrafAn FDA-approved living cell therapy and bioengineered skin substitute used in chronic wound care, including diabetic foot ulcers and venous leg ulcers.® (PMA P950032) is a living, bi-layered skin substitute that received FDAFDAThe U.S. Food and Drug Administration (FDA) decides whether drugs, biologics, and medical devices are safe and effective enough to be sold. expedited review authorization in 1995 and full federal approval in 1998 and 2000. It is not experimental. It is not unproven. The FDA's own pivotal clinical trial established the following, subsequently confirmed and strengthened by 25 years of real-world evidence:

60%

Reduction in amputation risk

(6.3% vs 15.6%, p=0.028)

75%

Reduction in osteomyelitis risk

(bone infection: 2.7% vs 10.4%, p=0.04)

2 weeks

Time to wound closure once

finally approved after 17-month denial

UnitedHealthcare denied Apligraf for 17 months — citing it as "not medically necessary" — while non-healing wounds progressed. The patient subsequently developed osteomyelitis. Pathology from the eventual amputation described bone demineralized to a consistency "cuttable with a scalpel." The bone infection that caused the amputation is precisely the outcome the FDA trial proved Apligraf reduces by 75%.

When Apligraf was finally approved, it closed the wounds in two weeks. This vindicates the standard UHC suppressed for 17 months and establishes the 17-month delay as the proximate cause of the harm — not the underlying condition.

The thread lawyers struggle to follow — stated plainly:

This is not a medical disagreement about whether a treatment works. The federal government resolved that question in 1995–2000. This is a documented, foreseeable causal chain:

- FDA proves Apligraf reduces bone infection risk by 75% and amputation risk by 60%.

- UHC denies Apligraf for 17 months, citing "not medically necessary."

- Patient develops bone infection severe enough to require amputation.

- UHC's own IRE overturn rate of 85.2% means the denial was almost certainly wrongful by the insurer's own statistical pattern.

- When Apligraf is finally approved, wounds close in two weeks — proving the standard was never in dispute, only the insurer's willingness to honor it.

The denial didn't just delay treatment. It denied a treatment the federal record proves prevents the exact harm that followed. That foreseeability is what distinguishes this from a coverage dispute.

See the remedy for this → Room III

The legal mandate these numbers violate — and the legislative architecture that closes the gap.